In General

The recent ban on exports of food and agricultural products from Iran—historically, the leading supplier of fresh fruit and vegetables to the GCC—has significantly contributed to the current vegetables supply shortage in the market. Fruit demand remains subdued, although pricing is medium to strong. Despite this lower general demand trend, key fruit categories such as lemons, grapes, plums, and bananas continue to perform strongly, maintaining high demand and price levels.

| 1.00 USD = 3.67 AED (Emirate Dirham) |

| 1.00 USD = 3.75 SAD (Saudi Riyals) |

| 1.00 USD = 122.74 BDT (Bangladeshi Taka) |

| 1.00 USD = 92.65 INR (Indian Rupees) |

| 1.00 USD = 16.43 ZAR (South African Rand) |

Citrus

There appears to be limited demand in the market for oranges and soft citrus, while lemons continue to perform well due to constrained arrivals.

South Africa

Lemon supply is showing gradual improvement as harvesting gains momentum across more regions. However, volumes are still not at full capacity.

Weather conditions in northern growing areas are still a factor, with intermittent rainfall continuing to affect harvesting and packing operations in the short term. Eastern Cape will start with small volumes. For the Middle East market, the big question remains how big a portion of the Senwes and Eastern Cape crop will be affected by CBS.

Market Prices (Dubai, Kuwait and Jeddah)

Pome

Apples and pears continue to trade at a slower pace. However, market dynamics are expected to shift in the coming weeks as South African supply—particularly of Royal Gala apples—begins to tighten with the transition from the Regular Atmosphere (RA) season to the Controlled Atmosphere (CA) season. This reduction in availability, combined with increased global demand from EU and UK retail programs, is likely to support a limited supply scenario which should support maintenance of high sales values, albeit at low movement rates.

Market Prices (Dubai, Kuwait and Jeddah)

Grape, Kiwi & Stone

Grapes

Seedless Grapes (Red & Black)

Supply is extremely limited, with the season nearing completion. Prices remain high due to tight availability.

Seeded Grapes

Seeded grapes are almost completely out of the market. Any remaining stock is trading at elevated price levels.

Kiwi

Supply is typically dominated by Iran supported by smaller volumes from Turkey. With Iranian product currently absent, a supply gap has opened, creating an opportunity for Chilean kiwi. However, pricing will be critical, as the market remains highly sensitive to cost, especially in the absence of competitively priced Iranian fruit.

Stone Fruit

Apricots

The apricot season remains unchanged, with no volumes available in the market.

Plums

The season is effectively finished, with only negligible volumes in circulation. Prices remain firm on any remaining good-quality stock.

Market Prices (Dubai, Kuwait and Jeddah)

India / Bangladesh

India

Blue skies

Blues skies in India mean that there are less people in the cities and that manufacturing/construction has slowed down. This is mainly due to the gas and fuel shortage. This has affected the buying power on all fruits. Selling prices on local mangoes dropped by 75% in one week due to less consumption. Movement of imported fruit has slowed down. There is currently a lot of RYB in the market that us putting pressure on the Flash Gala selling prices.

Bangladesh

Removal of Dhaka Street vendors/shops

Large arrivals of South African Royal Gala/Gala apples, this week, are placing significant pressure on market prices and slowing the clearing of containers in port.

In addition, recent police action in Dhaka has led to the removal of street vendor shops, which has had a major impact on sales.

These vendors account for approximately 90% of fruit distribution in the city, resulting in a sharp drop in overall market movement.

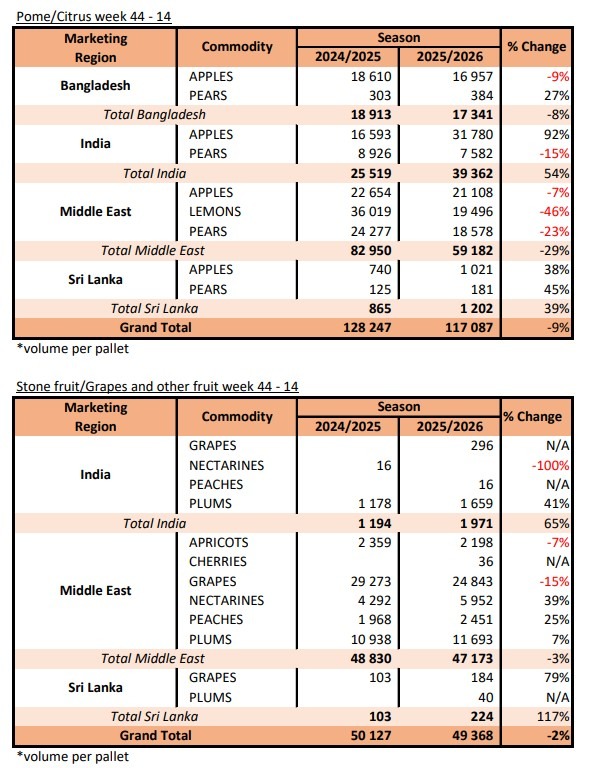

SA Statistics

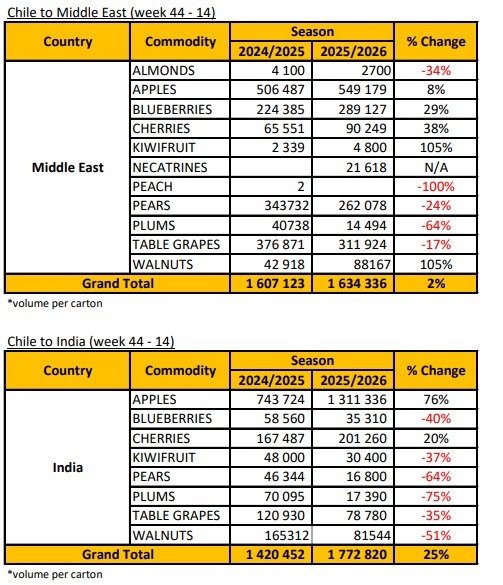

Decofrut Statistics

Follow links to our social pages