In General

Market activity across most commodities in the Middle East remains slow, driven by ongoing uncertainty and continued rising logistics costs across both sea and road freight. However, the market remains optimistic, particularly for the upcoming South African soft citrus season. This is largely supported by reduced availability from Morocco and China. There is also less volume from China, with ongoing disruptions linked to the closure of the Strait of Hormuz .

| 1.00 USD = 3.67 AED (Emirate Dirham) |

| 1.00 USD = 3.75 SAD (Saudi Riyals) |

| 1.00 USD = 122.72 BDT (Bangladeshi Taka) |

| 1.00 USD = 94.28 INR (Indian Rupees) |

| 1.00 USD = 16.64 ZAR (South African Rand) |

Citrus

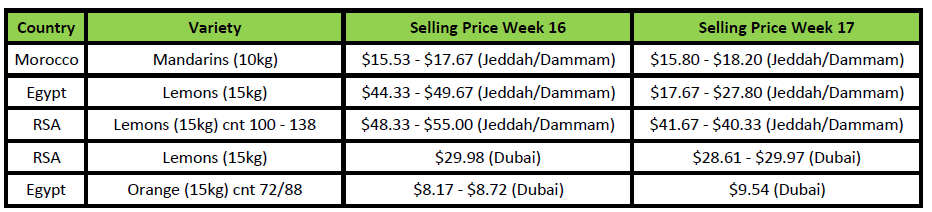

Last of the Egyptian Navels and Lemons are still available in the Saudi market, with large volumes of Egyptian Valencia oranges selling at average prices.

Prices for South African lemons are starting to come down as more volume is arriving each week.

South Africa

Lemon supply continues to improve gradually as more harvesting regions come into production. Volumes are increasing week-on-week, although the market has not yet reached peak supply levels.

Weather conditions in northern production areas remain a concern, with intermittent rainfall still causing minor disruptions to be harvesting and packing.

The Eastern Cape is now entering the market with early volumes, contributing to the overall increase in supply.

Market Prices (Dubai, Kuwait and Jeddah)

Pome

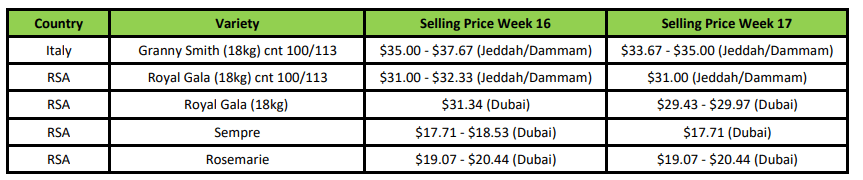

Demand for Royal Gala apples is still slow, there has been a noticeable increase in interest for Granny Smith apples due to limited availability from Italy, presenting a potential opportunity for South African supply. Pear sales remain under pressure, mainly due to an influx of arrivals following earlier port congestion, which resulted in delayed shipments entering the market simultaneously.

Market Prices (Dubai, Kuwait and Jeddah)

Grape, Stone & Kiwi

Grapes

Seedless Grapes (Red & Black)

Prices remain elevated where stock is still available, but trading activity is minimal.

Seeded Grapes

Red Globe grapes saw price decreases this week due to the arrival of new volumes from Peru.

Stone Fruit

Plums

Prices continue to trend downward as the market adjusts to current stock levels.

Kiwi

Kiwi fruit availability remains limited. Iran continues to supply limited volume via overland routes, with product being repacked and re-exported through Syria into Saudi Arabia. Despite this, there is still a potential opportunity for Chilean kiwi fruit, provided pricing remains competitive.

Market Prices (Dubai, Kuwait and Jeddah)

India / Bangladesh

India

Citrus

Chinese late mandarins still dominate the market at low prices and are expected to be in the market for the foreseeable future.

Bangladesh

No report.

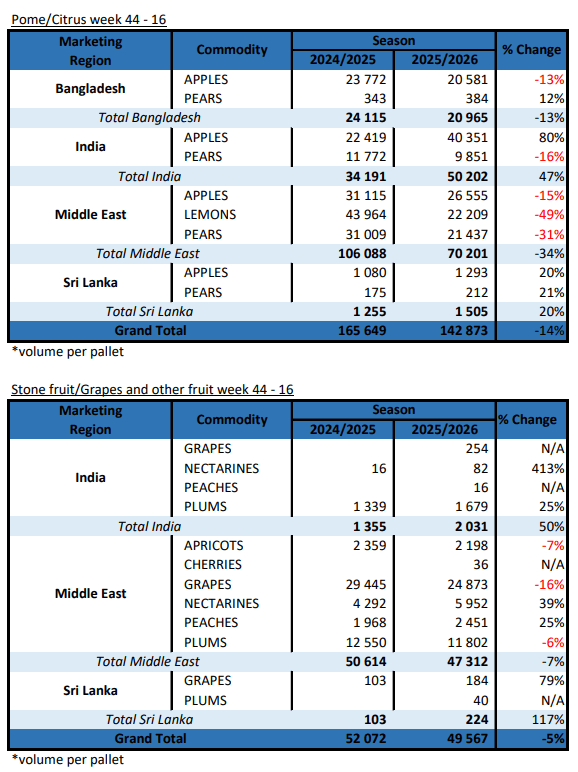

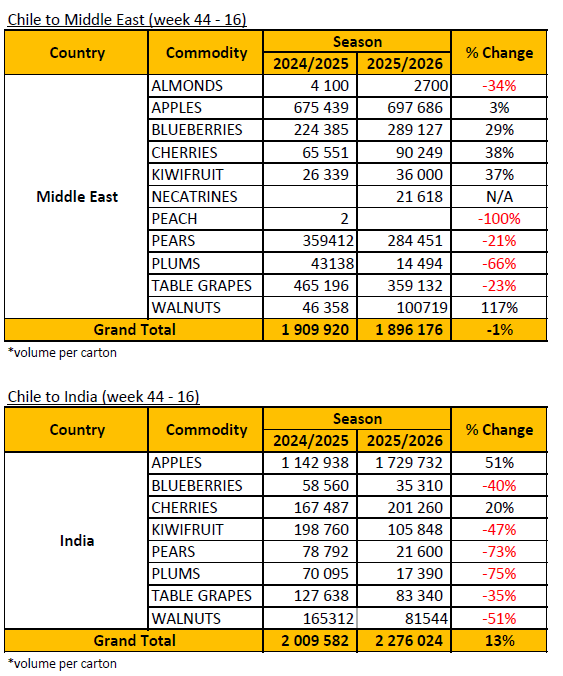

SA Statistics

Decofrut Statistics

Follow links to our social pages