In General

Congestion at Jeddah and Khor Fakkan Port remains a significant challenge, with a large number of containers still experiencing delays, creating a bottleneck throughout the supply chain. Although containers continue to be cleared periodically, the situation is further complicated by a critical shortage of reefer trucks, which is restricting the movement of cargo from the port.

These factors have led to irregular product supply in the market, resulting in significant price volatility. The combination of port congestion, uneven container clearances, and limited refrigerated transport capacity makes it challenging to accurately interpret current market conditions or forecast price trends.

Overall, the Middle East fruit market remains heavily influenced by logistical constraints and inconsistent supply patterns.

| 1.00 USD = 3.67 AED (Emirate Dirham) |

| 1.00 USD = 3.75 SAD (Saudi Riyals) |

| 1.00 USD = 122.79 BDT (Bangladeshi Taka) |

| 1.00 USD = 95.37 INR (Indian Rupees) |

| 1.00 USD = 16.31 ZAR (South African Rand) |

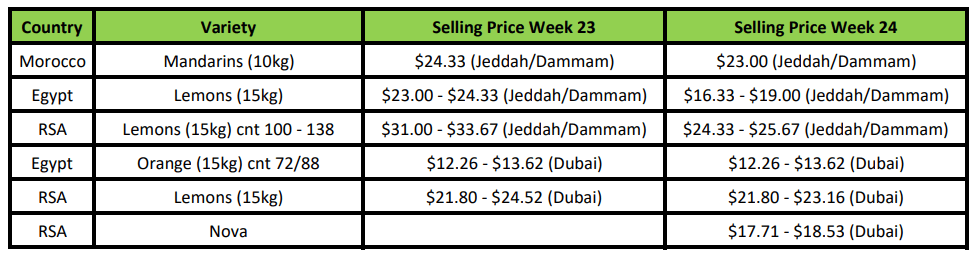

Citrus

Lemons

Lemon supply continued to increase as additional Southern Hemisphere volumes entered Middle East markets. Availability improved further during the week, resulting in lower sales prices. Market prices declined more this week more lemons available in the market.

Oranges

Egyptian Valencia oranges remained widely available across the market, with supply levels sufficient to meet current demand requirements. Pricing remained largely stable.

Market Prices (Dubai, Kuwait and Jeddah)

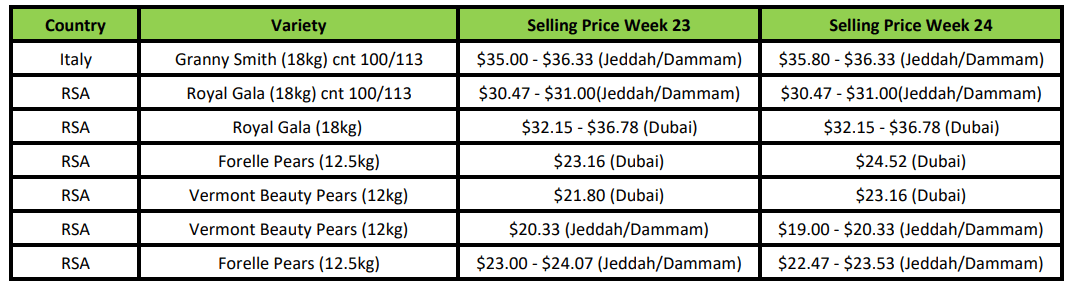

Pome

From South Africa, pear shipments to the Middle East are down 32% compared with the same period last season. This supply shortfall is not expected to be recovered during the remainder of the season, meaning the market is likely to continue experiencing reduced pear availability on a week-to-week basis. This should lead to a favourable pear market in coming weeks.

Apple exports from South Africa to the Middle East are also lower, with volumes down 9% compared to the same period last year. Despite the reduced supply, apple prices have remained relatively stable. However, overall consumption levels are below normal, resulting in slower market activity .

Market Prices (Dubai, Kuwait and Jeddah)

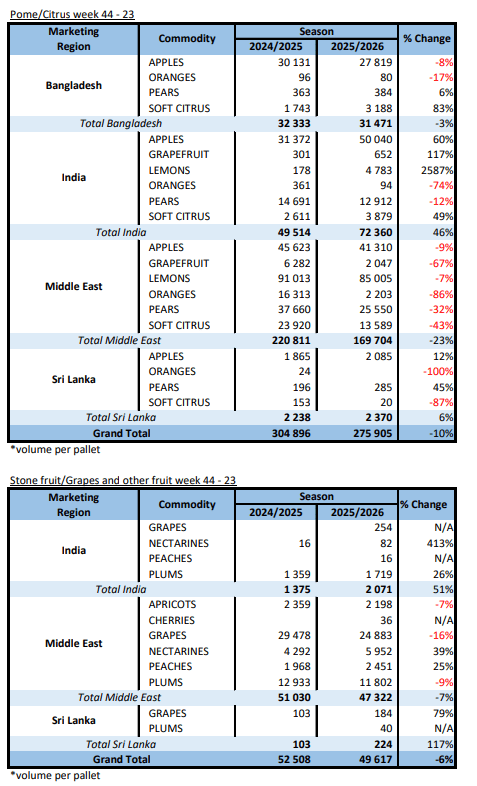

Grape, Stone & Kiwi

Grapes

Seedless Grapes (Red & Black)

Seedless grape prices remained under pressure this week as market inventories continued to weigh on trading conditions. Demand was steady, although buyers remained selective, focusing on fresher arrivals and higher-quality fruit. Market activity was moderate, with competition increasing across wholesale channels.

Seeded Grapes

Red Globe grape supply remained steady following ongoing arrivals from Peru. Market availability continued at comfortable levels, maintaining competitive pricing across the region. Demand remained stable, supported by regular retail programmes and consistent consumer purchasing.

Stone Fruit

Plums

Plum trading remained relatively stable across the region, with supply levels continuing to support consistent market availability. Pricing on selected varieties remained under pressure, particularly where inventories were elevated, while demand continued to favour premium-grade fruit with strong colour and eating quality.

Kiwi

Chilean kiwifruit has begun arriving in the market. With Iranian kiwifruit currently absent, there appears to be a favourable window of opportunity for Chilean suppliers to establish a stronger market presence and benefit from reduced competition during this period.

Market Prices (Dubai, Kuwait and Jeddah)

India / Bangladesh

India

Apple

Apple demand and prices are increasing as less fruit is hipped from SA. Chile volumes still arriving.

Bangladesh

Apple Market

Importers are making a profit on apples as the market is performing well. No apples in market from other countries, therefore high demand for South African apples.

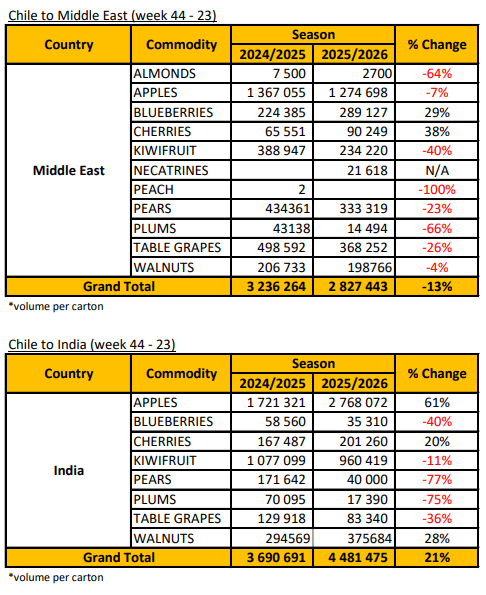

SA Statistics

Decofrut Statistics

Follow links to our social pages